How to Start a Private Limited Company Registration

The term accounting refers to a lot more than just bookkeeping. Accounting is a broad term that encompasses the entire issue area, whereas bookkeeping is a subset of accounting that employs accounting principles in its operations. Designing bookkeeping systems, implementing controls to maintain and operate the system, and analyzing any data are all important components of accounting.

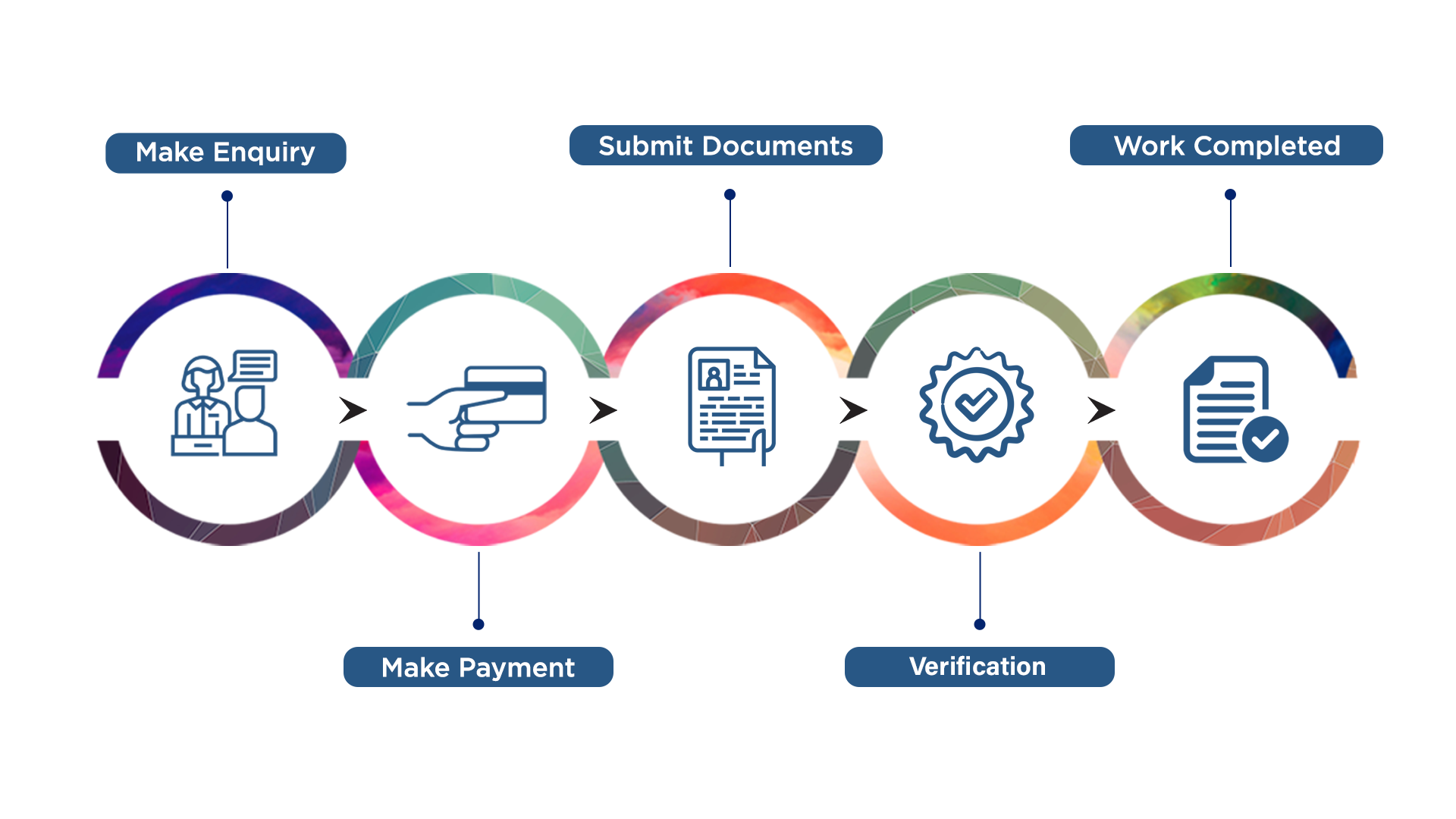

Package Inclusion :-

What exactly is accounting?

The term accounting refers to a lot more than just bookkeeping. Accounting is a broad term that encompasses the entire issue area, whereas bookkeeping is a subset of accounting that employs accounting principles in its operations. Designing bookkeeping systems, implementing controls to maintain and operate the system, and analyzing any data are all important components of accounting.

Accounting is mostly made up of the following components:

• Keeping track of spending.

• Creating financial statements for the entire organization. • Analyzing the operational costs.

• Taking care of tax returns.

• Assisting the company owner in understanding the financial consequences of his or her choices.

Accountancy Types

Accounting is divided into two types which are financial accounting and managerial accounting.

Accounting for Money

Financial accounting includes the preparation of accurate financial statements. Financial accounting's purpose is to measure a company's performance as accurately as possible. While financial statements are designed for use by third parties, they can also be utilized by internal management to help make decisions.

Accounting for Managers

Financial accounting gathers data, which is then analysed by managerial accounting. The process of creating financial reports on a company's operations is referred to as financial reporting. The management team uses the reports to assist them in making tactical decisions. Managerial accounting is a procedure that helps an organization to maximize efficiency by examining financial accounting, deciding on the best next steps, and then communicating those steps to all internal business management.

Accounting Methodologies

In general, there are two main ways to record financial transactions in accounting books:

1. Cash System: Financial transactions are not recorded in the records until the relevant cash amount is actually received or paid, according to the cash system. This method does not keep a complete record of financial transactions because credit transactions are not recorded, and therefore does not provide a true picture of profit and loss at any given point in time.

2. Accrual System: Financial transactions are documented in the books of accounts as and when they accrue during the period under this accounting system. This system provides a comprehensive picture of financial transactions made during the period since it records all transactions made during the period, regardless of whether cash was received or paid.

Accounting Theories

Separate business entity concept: When accounting for a company, we draw a clear difference between the company and its owner. All business transactions are kept track of from the perspective of the company rather than the owner. To the degree that he purchased capital, the proprietor is considered a creditor of the organization. Concept of a Double Entry: Every financial transaction necessitates the recording of two parts of accounting. For example, if a company sells items valued Rs. 5,000, this transaction necessitates the recording of two aspects of accounting. One is a 5,000-rupee stock reduction, while the other is a 5,000-rupee cash receipt. A double-entry system keeps track of these two components of a single transaction. The whole amount debited will always equal the total amount credited, according to this rule. The basic accounting equation for the above rule is: -Assets = Liabilities + Equity of Owners Concept of a going concern: Accounting expects that a firm will continue to function in the future for a longer period of time. In other words, it is assumed that the entity's business operations will not be curtailed unless it is absolutely necessary. The financial accounts of a company entity are prepared on this basis, and it is on this basis that investors agree to invest in the business. Concept of a matching: Revenues and expenses must be recorded at the same time as they are incurred, according to this notion. We match revenues to expenses incurred throughout the accounting period in general. In general, revenue gained during a time can only be quantified when it is compared to the expenses incurred during that period. When producing a period's financials, many adjustments are performed based on this notion for prepaid expenses, accruing incomes, and so on.

What is the definition of bookkeeping?

Isn't bookkeeping merely another term for accounting? Wrong. Many individuals mistakenly believe that the two jobs are interchangeable; however, bookkeeping refers to the daily recording of financial transactions and activities. It's a subset of accounting that necessitates the completion of the following tasks in order to develop a financially sound business: • Keeping track of financial transactions. • Debits and credits are recorded. • Creating invoices • Keeping track of current, historical, and general ledger balances and balancing them. • Payroll is being completed. One of the most crucial components of bookkeeping is managing a general ledger. This ledger contains all of a bookkeeper's records, costs, and receipts. Posting is the act of entering information into a ledger. As a result, the more sales, or expenditures there are, the more often the ledger will be updated.

Bookkeeping's Objectives

The following are the goals of bookkeeping:

• To keep track of the transactions The primary purpose of bookkeeping is to keep systematic records of all financial transactions that are precise and detailed. It maintains a systematic record of all transactions and ensures that all financial transactions are recorded in the books of accounts. These transactions can be referred to in the future.

• To demonstrate the proper location The total impact of a company's financial transactions can be determined with the help of bookkeeping. It measures the financial impact of all company transactions over the course of a fiscal year. It gives financial data to the company's owners and management, assisting them in the formulation of future policies and plans.

• Errors and scams must be detected. Bookkeeping aids in the identification of transactions and the chronological and methodical summarization of those transactions. It makes sure that the books of accounts are accurate, current, and comprehensive. As a result, it assists in the detection of any flaws or scams within the organization. Bookkeeping System Types There are two different sorts of accounting systems. Business organizations can choose from a variety of bookkeeping systems. Some organizations use both of these. There are two types of bookkeeping systems which are given below:

• Bookkeeping using a single-entry system The single-entry accounting system is a basic technique for recording daily receipts and generating a weekly or daily cash flow report for a business. In a single-entry accounting system, the bookkeeper records one entry for each transfer of funds or activity. In a single-entry accounting system, only one side of a transaction or activity is recorded. Purchases, cash receipts, payments, and sales are the only things it keeps track of. It is primarily used by small enterprises with few transactions.

• Bookkeeping with a double-entry system In the double-entry accounting approach, each financial transaction or is recorded twice. By recording the credit entry for each debit entry, the double entry system offers checks and balances. It is not a cash-based system, and only when income or debt is created, transactions are recorded. The double-entry bookkeeping method is based on the duality concept, which indicates that every financial transaction affects two accounts. Every debit entry to one account corresponds to a credit entry in another account, and vice versa. This approach is widely used and is thought to be accurate when it comes to recording commercial and financial transactions.

Bookkeeping's Objectives

The following are the goals of bookkeeping:

• To keep track of the transactions The primary purpose of bookkeeping is to keep systematic records of all financial transactions that are precise and detailed. It maintains a systematic record of all transactions and ensures that all financial transactions are recorded in the books of accounts. These transactions can be referred to in the future.

• To demonstrate the proper location The total impact of a company's financial transactions can be determined with the help of bookkeeping. It measures the financial impact of all company transactions over the course of a fiscal year. It gives financial data to the company's owners and management, assisting them in the formulation of future policies and plans.

• Errors and scams must be detected. Bookkeeping aids in the identification of transactions and the chronological and methodical summarization of those transactions. It makes sure that the books of accounts are accurate, current, and comprehensive. As a result, it assists in the detection of any flaws or scams within the organization. Bookkeeping System Types There are two different sorts of accounting systems. Business organizations can choose from a variety of bookkeeping systems. Some organizations use both of these. There are two types of bookkeeping systems which are given below:

• Bookkeeping using a single-entry system The single-entry accounting system is a basic technique for recording daily receipts and generating a weekly or daily cash flow report for a business. In a single-entry accounting system, the bookkeeper records one entry for each transfer of funds or activity. In a single-entry accounting system, only one side of a transaction or activity is recorded. Purchases, cash receipts, payments, and sales are the only things it keeps track of. It is primarily used by small enterprises with few transactions.

• Bookkeeping with a double-entry system In the double-entry accounting approach, each financial transaction or is recorded twice. By recording the credit entry for each debit entry, the double entry system offers checks and balances. It is not a cash-based system, and only when income or debt is created, transactions are recorded. The double-entry bookkeeping method is based on the duality concept, which indicates that every financial transaction affects two accounts. Every debit entry to one account corresponds to a credit entry in another account, and vice versa. This approach is widely used and is thought to be accurate when it comes to recording commercial and financial transactions.

Frequently asked questions:

1. What does a bookkeeper actually do?

A bookkeeper's main job is to keep track of a company's financial operations, such as purchases, sales, and expenses. These transactions are initially entered into a general ledger, which is then utilized to create a balance sheet.

2. What's the difference between bookkeeping and accounting?

Accounting covers a wide range of topics. It necessitates a better comprehension of bookkeeping records as well as the capacity to analyze and interpret the information contained in them. Accounting is concerned with the summary phase of an accounting system, whereas bookkeeping is concerned with the recording phase. Accounting begins where bookkeeping concludes, and bookkeeping provides the essential data for accounting.

3. Is it difficult to work as a bookkeeper?

No. Bookkeeping is a relatively simple and straightforward activity that may be picked up quickly while working.

4. What are the differences between the two types of bookkeeping?

Single-entry and double-entry bookkeeping are the two most popular methods of bookkeeping. Although each has its own set of advantages and disadvantages, the organization must select the one that best meets their requirements.

5. In accounting, what are the three types of accounts?

• Individual Account.

• Account that is real.

• Account Nominal.

\6. What exactly is the accounting cycle?

The accounting cycle is the process of a company's accounting events being identified, analysed, and recorded. It's an eight-step process that starts when a transaction occurs and finishes when the transaction is recorded in the financial statements.

7. In accounting, what is a flowchart?

Flowcharts can be created using a variety of software applications. An accounting flow chart is a type of diagram that depicts a process using various symbols that carry information about steps or business processes. It is designed primarily for the accounting and financial departments.

8. What is a petty cash book, exactly?

The petty cash book is a chronological record of small cash expenditures. The petty cash book is usually a physical ledger book rather than a digital record. As a result, the book is a manual record-keeping system.